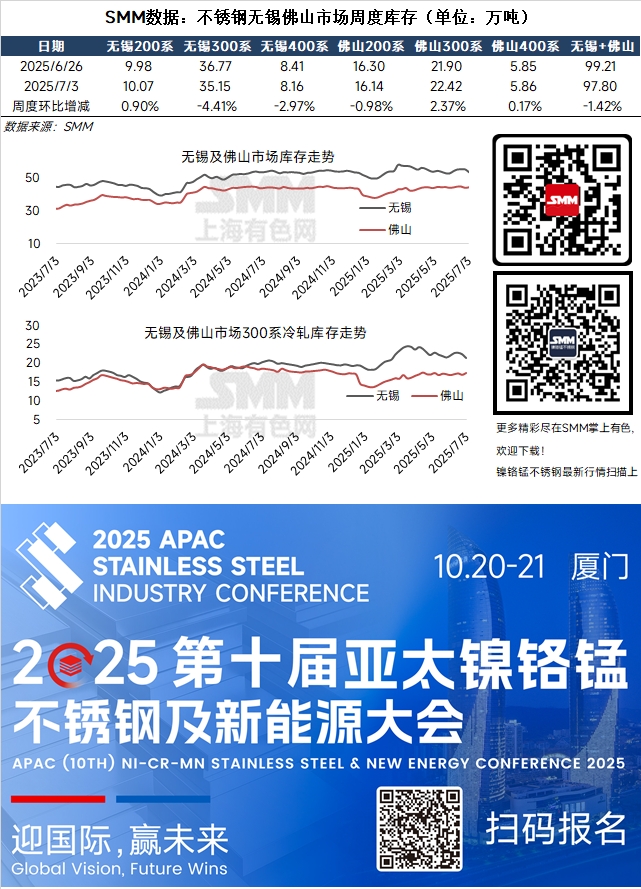

SMM reported on July 3 that during this week (June 27 - July 3, 2025), the total inventory in the two major stainless steel markets of Wuxi and Foshan continued to destock, dropping from 992,100 mt on June 26, 2025, to 978,000 mt on July 3, representing a 1.42% WoW decline.

At the beginning of this week, as the news of production cuts by stainless steel mills last week was gradually absorbed by the market, coupled with the cancellation of the flat plate price limit policy by a major stainless steel mill, market confidence was shaken, prices pulled back, and transactions became mediocre. However, starting from mid-week, driven by favorable macro policies and the "anti-cut-throat competition" news, the SS futures market regained strength, and spot market prices stopped falling and rebounded, with market inspection activities becoming more active. Traders, leveraging their low-cost inventory from earlier periods, had room for price concessions, releasing downstream demand that had been suppressed by pessimistic sentiment. Transaction conditions improved significantly during the week. Data showed that social inventory of stainless steel fell for two consecutive weeks, with a more pronounced decline this week. The stainless steel market remains in the off-season, with no significant recovery in downstream demand. Although production cuts by stainless steel mills have alleviated some supply pressure, the high inventory levels at in-plant and front-end warehouses still pose resistance to shipments. The volatile tug-of-war between longs and shorts in the market is expected to persist in the short term, requiring close attention to the progress of production cuts and the sustained impact of macro policies.

200-series: In Wuxi, 200-series inventory increased from 99,800 mt to 100,700 mt, a 0.9% rise; in Foshan, it decreased from 163,000 mt to 161,400 mt, a 0.98% drop. 300-series: In Wuxi, 300-series inventory fell from 367,700 mt to 351,500 mt, a 4.41% decline; in Foshan, it rose from 219,000 mt to 224,200 mt, a 2.37% increase. 400-series: In Wuxi, 400-series inventory decreased from 84,100 mt to 81,600 mt, a 2.97% drop; in Foshan, it increased from 58,500 mt to 58,600 mt, a 0.17% rise.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)